“The bumper returns offered by most asset classes in 2019 could tempt investors to think making money is easy but as master investor Warren Buffett once cautioned, ‘Speculation is most dangerous when it looks easiest.’

“Events in the Middle East are providing an unfortunate reminder that unexpected developments can still make financial markets pause for thought. A surge in the gold price toward $1,600 an ounce suggests that some investors are aware of the value of potential safe havens and this makes sense, because portfolio construction should focus on risk and downside protection as much as it does upon reward.

“With this year’s bumpy start in mind, it may therefore be worth investors taking time to consider what could go wrong in 2020. This is not to say that something will go wrong. But to casually assume that what has worked for the last ten years will provide a repeat performance in the 2020s could be dangerous. Investors might like to ensure they have balanced, diversified portfolios which can protect them, and profit, from a range of scenarios and not just one,” comments Russ Mould, investment director at AJ Bell.

“From a top-down perspective, five (unexpected) developments which could hit share prices in the year ahead include

• A spike in oil prices

• A break-down in the trade talks between the US and China

• Corporate profits disappoint

• Inflation picks up

• Interest rates rise (much faster than expected)

“Share prices trade off perception until reality intervenes and there are several things which could intrude and change investors’ rosy view of the world, after a year when low interest rates, low inflation, rampant share buybacks, merger and acquisition activity and looser fiscal policy in many countries provided the background for further positive performance from stocks and bonds.

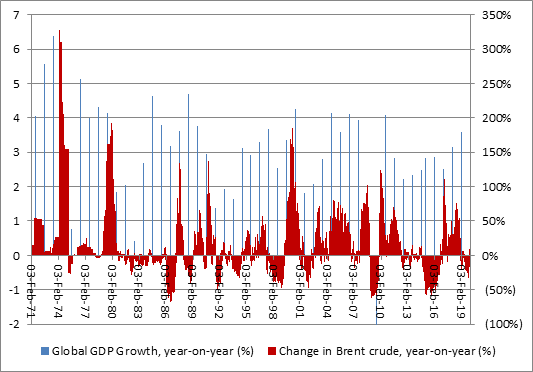

• Oil prices spike. This one does not seem quite so fanciful after America’s move to attack an Iranian general on Iraqi soil, as Brent crude has nudged its way toward the $70-a-barrel mark amid heightened tensions in the Middle East. History shows that if oil jumps by more than 50% year-on-year the global economy tends to slow and if it doubles then a recession is rarely far away, because of the hit to consumer spending power and corporations’ cost bases. (The good news here is that oil is basically flat on where it was a year ago and it would need to exceed $90 to rise by 50% so markets still have some leeway here).

Source: Refinitiv data

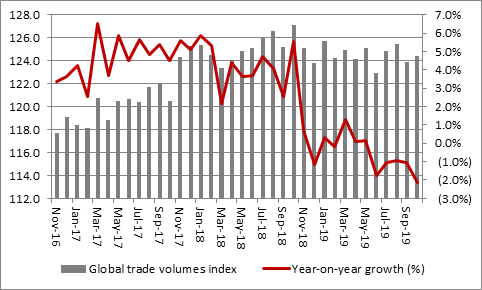

• US-China trade talks break down. One of the biggest sources of volatility has been the trade dispute between America and China. Hopes for a resolution – and a rolling back of tariffs – have grown, thanks to President Trump’s tweets that a ‘Phase One’ deal will be struck by 15 January. This leaves markets exposed to any delay or any moves by China to carry on regardless, especially on the vexed issue of its treatment of Western intellectual property. Data from the CPB in the Netherlands shows how global trade flows are slowing and industrial transportation equity indices are lagging (which is not normally a good sign), so an elongated disagreement between Washington and Beijing could be bad news.

Source: CPB World Trade Monitor, www.cpb.nl

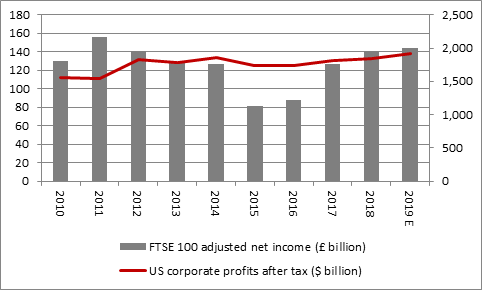

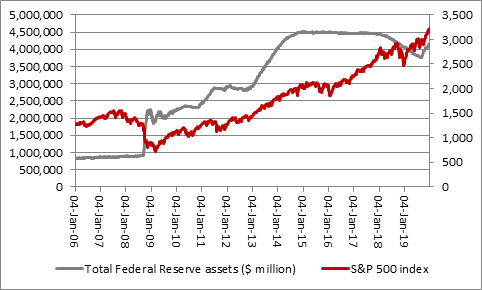

• Corporate earnings disappoint. One oddity of the equity bull run has been how modest profits growth has been, even as share prices have surged. America’s S&P 500 may have advanced by more than 20% last year but corporate earnings rose by just 4%, according to data from the Federal Reserve, whose numbers also suggest US private sector profits are not much higher than they were in 2012. (The implication is that share buybacks and financial engineering have therefore done a lot to goose earnings per share numbers). Aggregate earnings for the FTSE 100 were no lower in 2019 than they were in 2011, according to analysts’ estimates. This means valuations (the ‘p’ in price/earnings or PE calculations) have risen faster than the ‘e’ and that could leave share prices looking exposed if earnings start to disappoint – because of say a slump in trade or spike in oil.

Source: Sharecast, company accounts, FRED - St. Louis Federal Reserve database, Standard & Poor's, consensus analysts' forecasts

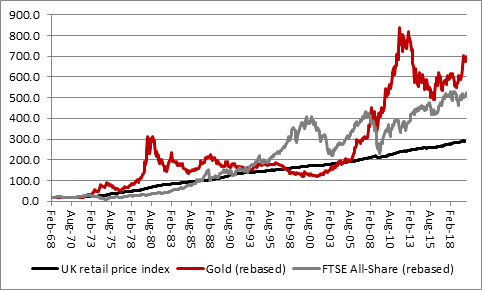

• Inflation. A low-growth, low-inflation, low-interest rate world has left investors scrabbling for yield and for returns better than cash for a decade, with equities a big winner as a result. Recent performance from bonds and equities alike suggests investors expect the next decade to offer more of the same so a spike in inflation could be a big surprise. Inflation would work against so many of the best strategies of the last ten or even 30 years – bonds, long-duration assets such as tech stocks – and force investors to reassess. The last real inflationary period was the 1970s when gold protected investors’ wealth in real terms and equities did not.

Source: Refinitiv data

• Tighter monetary policy. Since falling rates helped to persuade investors to look beyond cash in 2019 this would perhaps be the biggest surprise of all (and it would probably be preceded by an unexpected surge in inflation, which could perhaps result from ultra-loose monetary policy combined with a relaxation of fiscal policy). The Fed turned on the taps again in 2019 and it seems to have helped so it will be interesting to see what happens when the US central bank stops intervening in the overnight repo market.

Source: Refinitiv data, FRED – St. Louis Federal Reserve database