Almost £16 billion withdrawn from pensions since freedoms launched in April 2015 (latest HMRC statistics)

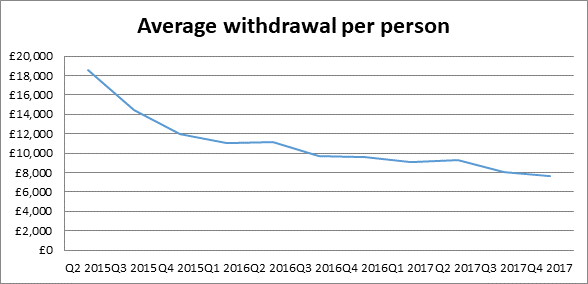

Average withdrawal per person hits new low of £7,596 in Q4 2017 (Q4 2016: £9,630)

Sustainability of withdrawals likely to be key focus of FCA Retirement Outcomes Review later this year – but no clear evidence of savers splurging their pension pots

Guidance amendment designed to boost take-up of Pension Wise needs urgent rethink

Tom Selby, senior analyst at AJ Bell, comments:

“HMRC’s latest figures once again demonstrate the enduring popularity of the pension freedoms, with 198,000 people taking flexible payments from their fund in the fourth quarter of 2017 – up from 162,000 in the same period a year earlier.

“Average withdrawals per quarter continue their downward trajectory, hitting a new low of £7,596 – more than £2,000 less than the figure recorded in Q4 2016. While this is not in itself evidence that savers aren’t at risk of making unsustainable withdrawals from their pensions, it equally isn’t a smoking gun requiring emergency regulatory or Government intervention.

“The sustainability of withdrawals and consumer engagement are central in the FCA’s Retirement Outcomes Review. Indeed our own research suggests many savers are entering drawdown simply to take their tax-free cash, without thinking properly about where their money is invested or how and when they are going to draw an income. Boosting engagement therefore needs to be a priority for policymakers across the FCA, Treasury, the DWP and TPR.

“While policymakers’ focus should remain razor sharp in boosting access to advice and guidance – as well as simplifying and improving communications sent to customers – any interventions in the drawdown market need to be based on the evidence available, rather than rhetoric.”

Financial Claims and Guidance Bill amendment

“In response to concerns about savers who don’t take financial advice making poorly informed decisions when entering drawdown, an amendment to the Financial Claims and Guidance Bill has been proposed which would require providers to book a Pension Wise appointment on behalf of customers.

“Although we believe the intention behind the amendment is laudable, it risks causing more harm than good. Placing a guidance barrier in the way of savers at the point they are accessing their pension – when they have already decided, possibly having already consulted Pension Wise, that they want the money – risks creating a tidal wave of complaints. It would be much better to nudge people to guidance before they have reached this point.

“Furthermore, it is not clear to us why ‘accessing the freedoms’ requires an automatic guidance appointment while buying an annuity does not. Alongside this, we remain entirely in the dark on how this will be implemented or what it will cost – one would imagine booking potentially hundreds of thousands of guidance appointments won’t come cheap. If providers are required to fund this, the extra cost will inevitably be worn by consumers.

“Boosting take-up of guidance and regulated advice is clearly a good thing, and would benefit providers like AJ Bell who actively compete in the open market.”